Japan SaaS Earnings Highlights (Part 1): Upward Guidance Revision by Plaid (TSE:4165) and Commentary on Financial Results of 6 Other SaaS Companies

Japan SaaS Earnings Highlights (Part 1): Upward Guidance Revision by Plaid (TSE:4165) and Commentary on Financial Results of 6 Other SaaS Companies

Table of Contents

Plaid (TSE: 4165): Upward guidance revision driven by enhanced customer success and more efficient use of servers

User Local (TSE: 3984): Looking for new revenue sources, leveraging stable growth

Rakus (TSE: 3923): RakuRaku statements continue to grow strongly, aiming for a 5-year revenue CAGR of 25-30%

oRo (TSE: 3983): ZAC license generates steady revenue; question remains if SaaS management platform becomes a new revenue source

Kaonavi (TSE: 4435): ARPU increase is driving overall growth; aiming for revenue of 10 billion yen (~100 million USD) in the medium term

HENNGE (TSE: 4475): ARR growth of 20% and focusing on ARPU increase to achieve further growth

AI inside (TSE: 4488): Growth slowed significantly due to non-renewal of contracts

This month there is a rush of financial results from SaaS companies. Last week, 15 SaaS companies announced their earnings.

In this article (part 1), we would like to report the highlights of the 7 companies, followed by the second article (part 2) covering the remaining 8 companies.

Plaid (TSE: 4165): Upward guidance revision driven by enhanced customer success and more efficient use of servers

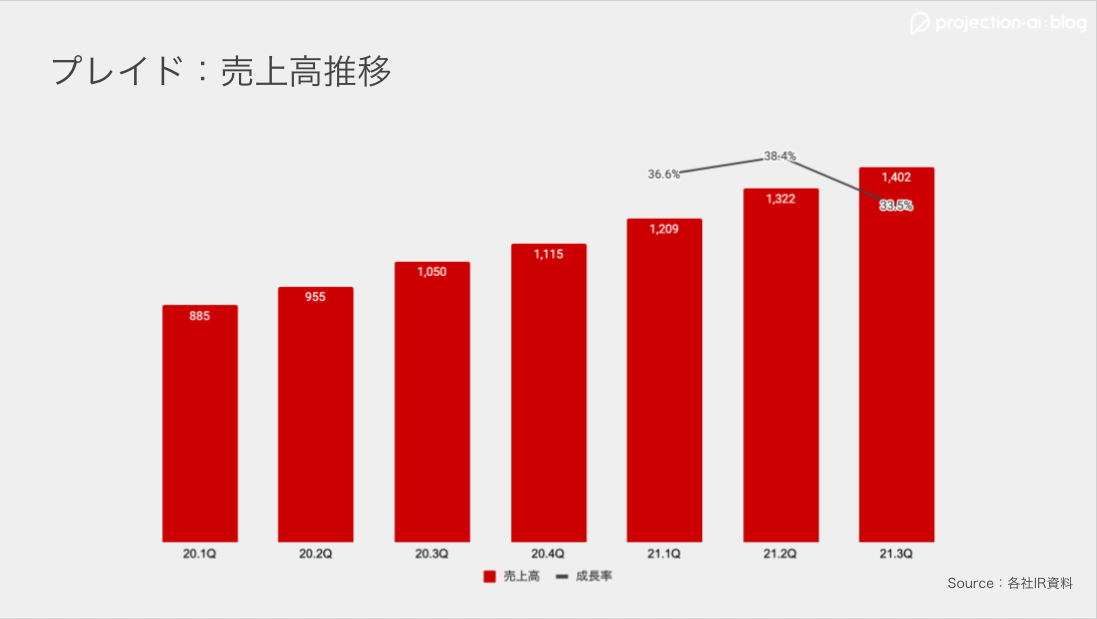

Plaid, a provider of the CX platform "KARTE", announced its FY21 3Q financial results on August 10, 2021.

Quarterly revenue grew 33.5% YoY to 1.4 billion yen (~14 million USD) , continuing the growth of over 30%. The company posted an operating profit of 88 million yen (~0.88 million USD) .

ARR (annual recurring revenue), which is an important metric for SaaS companies, grew 32.6% YoY to 5.43 billion yen (~54 million USD). Breaking down ARR, we observed that the number of customers grew 14.1% YoY to 517, and the unit price per customer grew 16.2% YoY to 874,000 yen (~87,400 USD), indicating balanced growth in both areas.

The company has strengthened customer success, resulting in strong upsell and cross-sell. In addition, the company maintained a good NRR of 113.7%, up 2.2 ppt from the previous quarter.

It is also worth noting that the gross margin has been improving. Efficient use of servers resulted in a gross margin of 74.2%.

SG&A expenses are expected to exceed the initial forecast due to accelerated investment, but operating profit is expected to be significantly higher due to higher revenue and gross profit. As a result, the company has revised their guidance upward for net revenue by 4.3%, gross profit by 7.6%, and operating profit by 504.8%.

The market perceived the earnings release positively and the stock price was up 8.1% from the previous day.

User Local (TSE: 3984): Looking for new revenue sources, leveraging stable growth

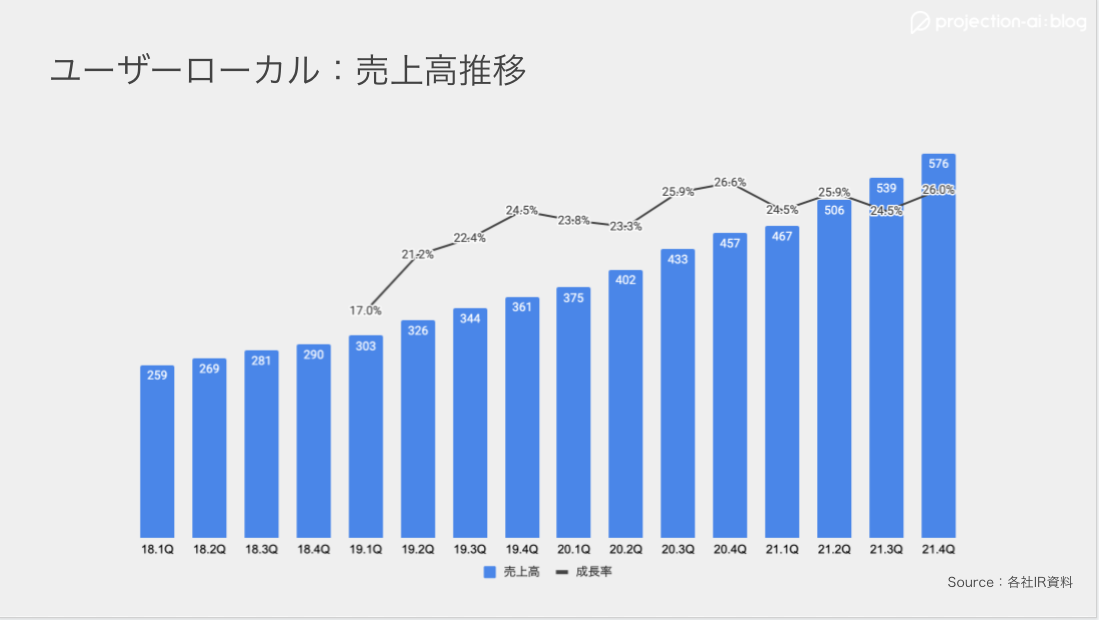

User Local, a big data analysis company, announced its FY21 4Q financial results on August 10, 2021.

Quarterly revenue continued to grow at a stable double-digit rate, up 26% YoY to 580 million yen (~5.8 million USD). For the full fiscal year, revenue was 2.08 billion yen (~20.8 million USD) (+25.2% YoY) and operating profit was 850 million yen (~8.5 million USD) (+24.4% YoY).

Currently, the company provides "User Insight" for website access analysis, "Social Insight" to support SNS operation and analysis, and "Support Chatbot", an AI-based chatbot, and will be expanding its services into new areas.

As a first step, the company has started providing "Cheating Deterrent AI" to prevent cheating in examinations and "Personal Information Anonymous Processing AI" to automatically anonymize personal information contained in electronic documents. In the future, the company plans to cover a wide range of areas such as automatic document processing, robot control, and sales support.

In order to strengthen its AI offerings, the company has been enhancing its recruiting effort. As a result, 70% of all engineers are now AI engineers.

Rakus (TSE: 3923): RakuRaku statements continue to grow strongly, aiming for a 5-year revenue CAGR of 25-30%

Rakus, a provider of cloud-based expense reimbursement software, announced its FY22 1Q financial results on August 12, 2021.

Quarterly revenue grew 33.3% YoY to 4.61 billion yen (~46.1 million USD), and operating profit declined 42.9% YoY to 520 million yen (~5.2 million USD).

The decline in profit was due to aggressive investments as the company expected, with the largest advertising spend ever in 1Q, increased rent for office expansion, and increased outsourcing costs being the main reasons for the increase in SG&A expenses.

Revenue in the cloud computing business continued to grow strongly with 37.9% YoY to 3.71 billion yen (~37.1 million USD). The ratio of recurring revenue to total revenue remains high at 92.1%.

Revenue of the mainstay "Raku Raku Seisan" led the overall growth at 39.3% YoY to 1.68 billion yen (~16.8 million USD). “Raku Raku Meisai”, which makes it easy to issue forms, is growing rapidly, with revenue up 110.9% YoY to 450 million yen (~4.5 million USD).

The company's five-year plan is to achieve a revenue CAGR of 25-30%, FY26 net income of over 10 billion yen (~100 million USD), and net assets of over 20 billion yen (~200 million USD). The plan is to grow the top line through aggressive investments in the first four years and harvest the investment in the last year. In addition, the company plans to aggressively conduct M&A in the cloud computing domain.

oRo (TSE: 3983): ZAC license generates steady revenue; question remains if SaaS management platform becomes a new revenue source

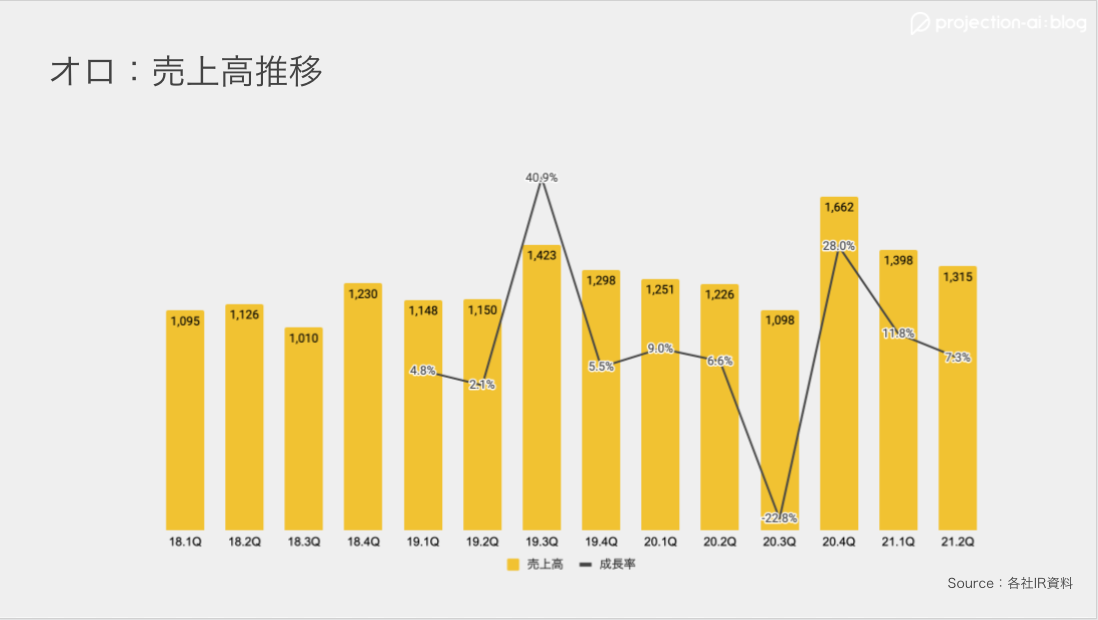

ORO, a company engaged in cloud ERP and other services, announced its FY21 2Q financial results on August 12, 2021.

Quarterly revenue grew 7.3% YoY to 1.32 billion yen (~13.2 million USD), and operating profit increased 30.5% YoY to 420 million yen (~4.2 million USD).

The number of licenses for the cloud ERP "ZAC", the main service, increased steadily by 14.5% YoY to 213,000.

The company's initiatives for this fiscal year include UIUX improvement, support for multiple languages and currencies, and development of new functions. As the company is also engaged in the digital transformation business, which supports corporate digital strategies, it is likely to apply the know-how it has cultivated in this area to its cloud business.

As a new initiative, the company also released the alpha version of its SaaS management platform "dexeco". With remote work taking root, many companies are now using SaaS. However, there may be situations where the SaaS is introduced, but not used at all and only costs are incurred. The company’s dexeco is expected to help manage these costs for SaaS services by analyzing SaaS services being used and their ROI. It seems that many SaaS for SaaS products have been born in Japan, so it will be interesting to see how the company will grow this product.

Kaonavi (TSE: 4435): ARPU increase is driving overall growth; aiming for revenue of 10 billion yen (~100 million USD) in the medium term

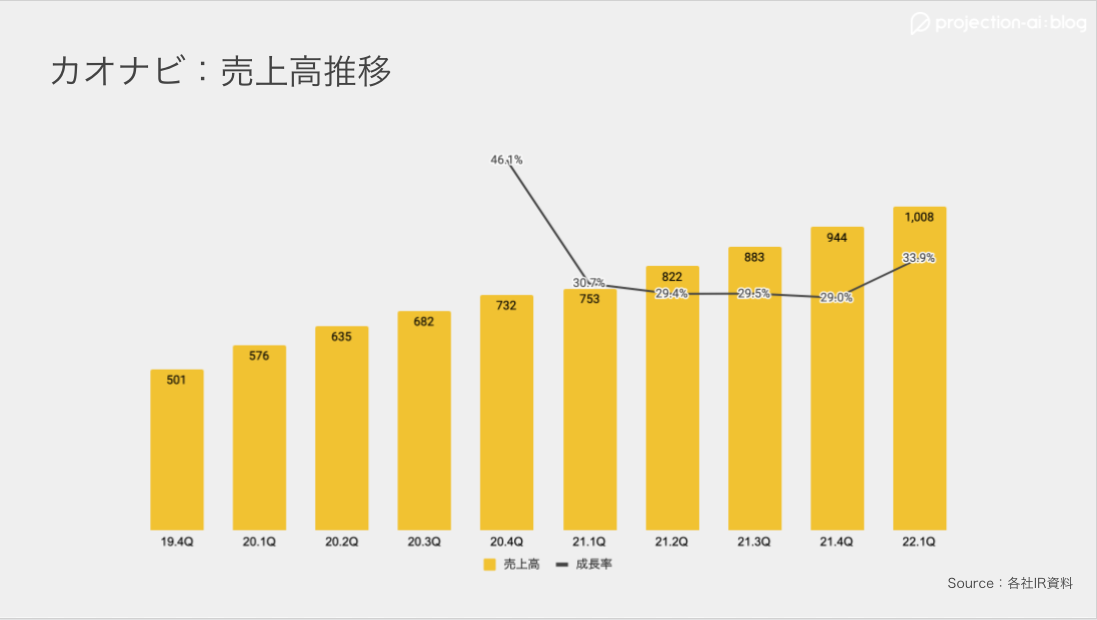

Khaonavi, a provider of talent management systems, announced its FY22 1Q financial results on August 12, 2021.

Quarterly revenue was 1.01 billion yen (~10.1 million USD) with 33.9% YoY, and operating profit was 30 million yen (~0.3 million USD), down 75.2% YoY. The recurring revenue % remained high at 88.2%.

The number of companies using the service increased by 15.2% YoY to 2,122, and ARPU increased by 19.25% YoY to 150,000 yen (~1,500 USD) , indicating that ARPU increase is driving overall growth.

The gross revenue churn rate remained at a low level of 0.69%. In addition to strengthening customer success, this is due to the fact that the more data is accumulated, the more difficult it is to churn.

LTV (lifetime revenue per customer) to CAC (cost per customer acquisition) has been on an upward trend since last quarter and is currently at 5.1x (more than 3x is considered healthy).

The company's medium-term plan (about five years) is to achieve revenue of 10 billion yen (~100 million USD), gross margin of 80%, and operating margin of 30%. It will be worth paying attention to how the company plans to achieve these goals.

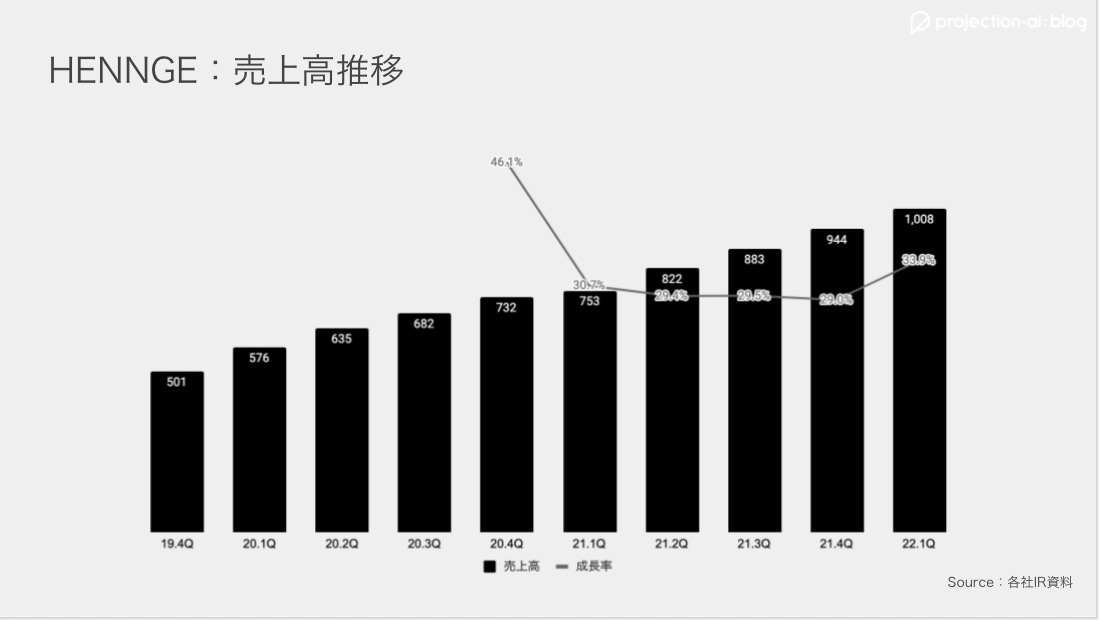

HENNGE (TSE: 4475): ARR growth of 20% and focusing on ARPU increase to achieve further growth

HENNGE, a provider of IDaaS, announced its FY21 3Q financial results on August 12, 2021.

Quarterly revenue was up 16.6% YoY to 1.23 billion yen (~12.3 million USD), and operating profit was up 30.9% YoY to 250 million yen (~2.5 million USD). The recurring revenue % remained at a very high level of 97.6%.

ARR for “HENNGE One”, the company's mainstay service, was up 20% YoY at 4.55 billion yen (~45.5 million USD). The number of subscribing companies increased by 18% YoY to 1,900, and the number of users increased by 8.4% YoY to 2.07 million, showing a steady increase in users.

The churn rate is quite low at 0.24%, and since IDaaS is generally used by the entire company, it is difficult for companies to churn once it is introduced, though it depends on the size of the company.

In order to maximize ARR, the company will focus on increasing the number of subscribers in the short term and increasing ARPU in the medium to long term.

In order to increase the number of subscribers, the company is focusing on online events. In the second half of the year, the company plans to hold four times as many events as last year.

As for the increase in ARPU, the company plans to add value by implementing new functions such as more secure file sending and receiving and enhanced security for access from smartphones. The company will also revamp its pricing plans in line with the functional development. By offering a plan for light users, the company aims to reach out to a wide range of users.

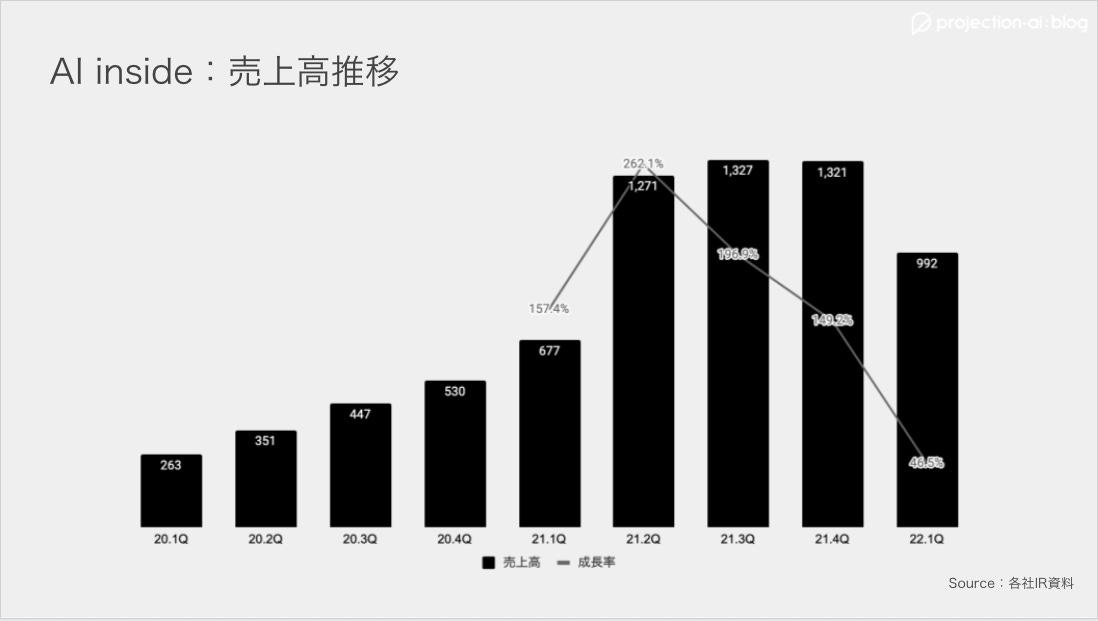

AI inside (TSE: 4488): Growth slowed significantly due to non-renewal of contracts

AI inside, a provider of OCR services using AI, announced its FY22 1Q financial results on August 12, 2021.

Quarterly revenue grew 46.5% YoY to 990 million yen (~9.9 million USD), and operating profit grew 27.2% YoY to 270 million yen (~2.7 million USD). The recurring revenue % remained high at 92%.

Considering that the company had been doubling its revenue, it is undeniable that growth has slowed down significantly. One of the reasons for this is that most of the "Omakase AI-OCR" licenses provided to NTT West on an OEM basis were not renewed.

There were 9,284 licenses for this service in the previous quarter, but the number has dropped significantly to 143 now. According to the company, the non-renewal cases have now been sorted out.

The number of users increased by 26.6% YoY to 29,237, but decreased by 24.3% QoQ, again largely due to Omakase AI-OCR.

The gross revenue churn rate excluding Omakase AI-OCR has remained low at 0.49%.

For the current fiscal year, the company is forecasting a significant decline in both sales and profit, with sales of 3.61 billion yen (~36.1 million USD) (-27.4% YoY) and operating profit of 450 million yen (~4.5 million USD) (-421% YoY).

Benefiting from remote work, the company's stock price temporarily rose to about 7 times from when it was listed. However, after the release of the non-renewal of the contract by NTT West, the stock price plummeted. It has now fallen to about one-tenth of its peak, and has also broken its initial price. The question now is whether the company can regain the trust of the market.

That’s all for now and will come back with the remaining 8 companies in the second article (part 2).

If you want to know more about SaaS companies in Japan, please subscribe and visit projection-ai:db!